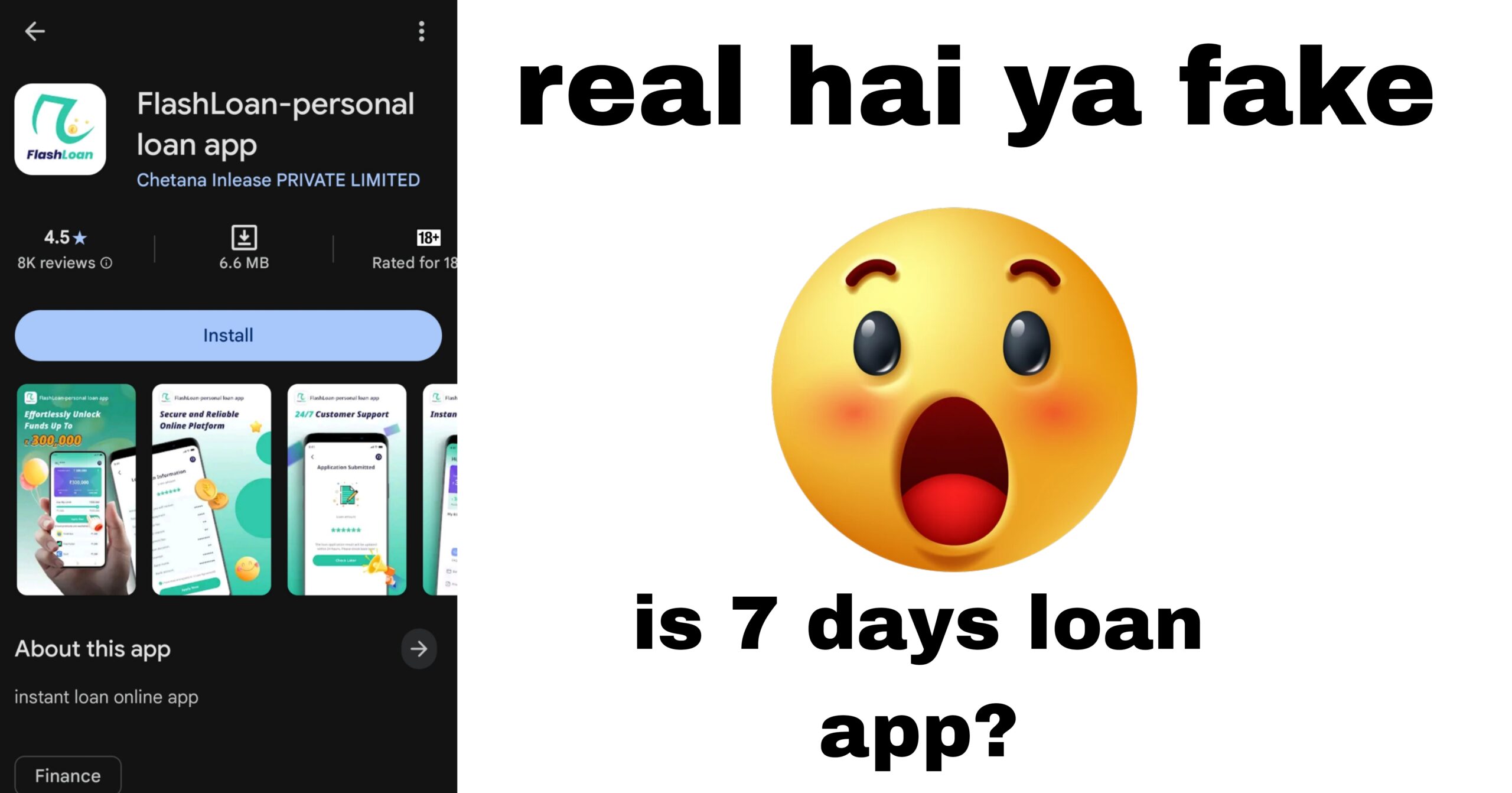

Flash Loan App Review 2025 : Flash Loan App Real or Fake?

In the age of digital finance, instant loan apps have become increasingly popular, promising quick access to funds with minimal paperwork. Among these is the Flash Loan App Personal Loan App, which markets itself as an ideal solution for fast, secure, and affordable personal loans. However, user reviews and industry insights raise serious concerns about … Read more