Credit Swift Loan App Review : Credit Swift Loan Real or Fake?

ek aisa 7-day loan app hai jo India mein bahut tezi se promote ho raha hai, lekin iske baare mein bahut saare critical reviews aur complaints Play Store aur online forums pe dikhai de rahe hain. Ye app claim karta hai ki ye fast aur flexible credit deta hai, lekin real users ke experiences se pata chalta hai ki ye bahut heavy charges lagata hai, scam jaise behave karta hai, aur logon ko lootne ka kaam karta hai.

Agar aap is app ke baare mein soch rahe ho ya already use kar chuke ho, toh please dhyan se padhiye. Main is article mein bilkul sachai ke saath bataunga ki Credit Swift kya hai, iske hidden charges kya hain, users ke real reviews kya keh rahe hain, aur agar aapke saath fraud ho gaya toh complaint kaise karen.

Credit Swift App Kya Hai? (Overview)

Credit Swift (Play Store link: https://play.google.com/store/apps/details?id=com.global.enterprise.fintech.runtime.core) ek instant personal loan app hai jo small amounts (jaise Rs 5,000 se Rs 50,000 tak) jaldi disburse karne ka promise karta hai. Ye revolving credit platform kehte hain, matlab aapko flexible funds milte hain. App ka rating Play Store pe around 4.5 stars dikhta hai, lekin ye rating mostly fake ya paid reviews se boost kiya gaya lagta hai.

App description mein ye bolta hai ki simple process hai, no paperwork, quick approval, aur urgent needs ke liye best. Lekin asli picture bilkul alag hai. Ye ek typical 7-day loan app hai, jisme loan short term (7 days ya kam) ke liye hota hai, lekin interest aur processing fees itne high hote hain ki repayment double ya triple ho jata hai.

Heavy Charges Aur Hidden Fees – Ye Sabse Bada Issue Hai

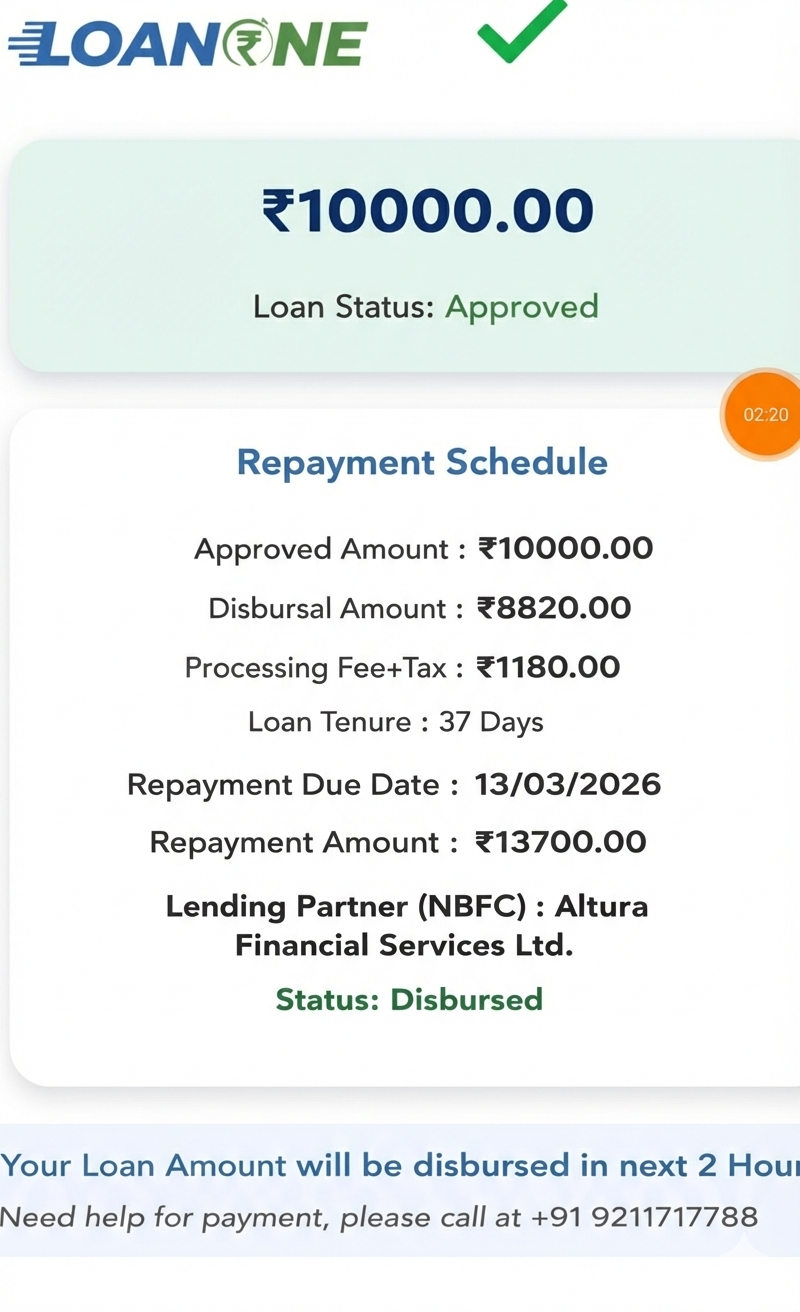

Is app mein jo sabse badi problem hai wo hai bahut heavy charges. Users kehte hain ki app dikhata hai loan Rs 12,000 approve hua, lekin actual mein sirf Rs 7,100 ya kam account mein aata hai. Fir repayment mein full Rs 12,000 + extra charges maangte hain within 7 days.

Example se samjhiye:

- Loan offer: Rs 12,000

- Disbursed amount: Rs 7,100 (deduction processing fee, interest advance mein kat jaata hai)

- Repayment: Rs 12,000 within 7 days

Ye effective interest rate 100-200%+ monthly ban jata hai, jo illegal hai RBI guidelines ke according. Normal RBI-approved apps mein interest 2-3% per month hota hai, lekin ye apps hidden fees, GST extra, aur penalty se loot lete hain.

Bahut se users complain karte hain ki ye app old banned apps ka clone hai. Ek review mein clearly likha hai: “This is the 7 days loan app guys… this old app was removed from play store again it created new one and the old data is cloned in this. Please don’t apply for this.”

Play Store Critical Reviews – Users Ki Real Kahani

App description pe bharosa mat kijiye, balki critical reviews pe focus kijiye jo Play Store pe milte hain (March 2026 ke around ke reviews se):

- Pradeep Pathak (05/03/26): “This is a very big scammer app, they are looting many people… showing loan of Rs 12000, out of which Rs 7100 deposited… pay Rs 12000 within 7 days. Very big scammer app.” (2 logon ne helpful bola)

- Amit R (09/03/26): “Not able to provide small loans at urgent times. Always showing denied whenever applied for loan.”

- Pokka Abhishaik (04/03/26): “This is the 7 days loan app guys… old app removed from play store, new one created, old data cloned… please don’t apply.” (3 logon ne helpful bola)

- VeeR Singh (08/03/26): “Only collecting data… worst and fake loan app.”

- Vishnumaya (08/03/26): Positive review tha, lekin jaise positive reviews paid ya fake lagte hain.

Aur bahut se similar reviews hain jahan log keh rahe hain data collection ke liye app use kar rahe hain, loan deny karte hain, ya harass karte hain repayment ke time.

Online search se bhi pata chalta hai ki similar names jaise Cred Swift, Swift Loan etc pe fraud complaints hain – morphed photos bhejna, contacts ko threaten karna, unauthorized loans disburse karna.

Ye sab typical fake loan app scam hai jo RBI ke rules follow nahi karte, unregistered NBFC hote hain, aur harassment karte hain.

Kyun Avoid Karna Chahiye Credit Swift?

- High Interest & Fees: 7 days mein double payment maangte hain.

- Scam Tactics: Loan approve dikhakar kam paise dete hain, fir full + extra maangte.

- Data Theft: App permissions se contacts, photos access karte, blackmail ke liye use.

- Clone App: Old banned apps ka new version.

- No RBI Approval: Real regulated apps RBI ke list mein hote hain (Sachet portal pe check karo), ye nahi hai.

- Harassment Reports: Threats, morphed images share karna common hai in jaise apps mein.

Agar aap urgent loan chahiye toh RBI-approved apps jaise MoneyTap, PaySense, CASHe, ya banks ke apps use kijiye. Unme interest low hota hai aur safe.

FAQ – Credit Swift Loan App Ke Baare Mein Common Questions

Q1: Credit Swift real hai ya fake?

A: Ye real app Play Store pe hai, lekin bahut saare users isko scam bol rahe hain high charges, harassment, aur fraud ke wajah se. Avoid karna better hai.

Q2: Isme interest kitna lagta hai?

A: Official description mein low batate hain, lekin real mein effective rate bahut high (100%+ per month) hidden fees se.

Q3: Loan apply karne se pehle kya check karna chahiye?

A: Play Store reviews padho (critical wale), RBI Sachet portal pe check karo app regulated hai ya nahi, aur friends se poochho.

Q4: App se loan mila toh repayment kaise?

A: 7 days mein full amount + charges. Late hue toh penalty aur harassment shuru.

Q5: Positive reviews kyun hain agar scam hai?

A: Bahut se fake ya paid reviews hote hain rating boost karne ke liye.

Q6: Safe alternatives kaun se hain?

A: RBI-approved NBFC apps jaise Navi, KreditBee (regulated), ya bank apps.

Agar Aapke Saath Fraud Hua Hai To Complaint Kaise Karen? (Step-by-Step Process)

Agar aapne Credit Swift ya similar app se loan liya aur fraud feel ho raha hai (harassment, morphed photos, unauthorized deduction, etc.), turant action lo:

- Sabse Pehle App Uninstall Karo: Phone se delete kar do, data access band karne ke liye.

- Evidence Collect Karo: Screenshots of chats, threats, transactions, bank statements, app messages – sab save karo.

- National Cyber Crime Helpline Call Karo: Dial 1930 (24×7 free). Financial fraud report karo, wo guide karenge.

- Online Report Karo: Jaao https://cybercrime.gov.in pe. “Report Other Cybercrimes” ya “Financial Fraud” select karo. Details fill karo, evidence upload karo. Complaint track kar sakte ho.

- Bank Ko Inform Karo: Agar unauthorized transaction hua toh bank se dispute raise karo, freeze karwao agar possible.

- RBI Complaint (Agar Regulated Lagta Hai): Pehle app/company se complain karo, fir RBI CMS portal https://cms.rbi.org.in pe file karo. Lekin in jaise apps mostly unregulated hote hain, toh cyber crime better.

- Local Police/Cyber Cell: Nearest police station ya cyber cell mein FIR file karo, especially agar threats ya blackmail hai.

- Google Play Store Pe Report Karo: App ko “Report” karo as spam/fraud.

Yaad rakho: Jaldi report karo toh chances zyada hain recovery ke aur harassment rukne ke. Government ab strict hai fake loan apps pe, bahut se ban ho chuke hain.

Final Advice: Credit Swift jaise 7-day loan apps se door raho. Emergency mein family/friends se help lo ya genuine sources use karo. Apni safety aur paise dono important hain. Agar koi doubt ho toh comment mein poochho!