VeyoCredit – Personal Credit App Review: VeyoCredit Loan App

Aaj kal India mein bahut saare log instant loan apps use kar rahe hain, especially jab emergency cash ki zarurat padti hai. Ek aisa hi app hai VeyoCredit – Personal Credit, jo Google Play Store pe available hai (package id: com.adisutomo.veyo). Ye app dikhta toh bahut attractive hai – 4.6 stars rating ke saath, easy personal credit aur loan options claim karta hai. Lekin users ke real reviews dekh kar lagta hai ki ye ek typical 7-day loan app hai jo bahut heavy charges lagati hai aur bahut se logon ne ise fraud ya scam bola hai.

Is article mein hum bilkul honest review denge VeyoCredit app ka. Hum app ke official description pe zyada bharosa nahi kar rahe, balki Play Store ke critical reviews aur users ke experiences pe focus kar rahe hain jo February 2026 ke around ke hain. Ye app Indonesia based developer (Adi Sutomo) ka hai, aur India mein bahut se logon ne isse related complaints ki hain jaise unauthorized loan credit, high repayment demands, blackmail via WhatsApp, aur data collection ke naam pe fraud.

VeyoCredit App Kya Hai Aur Kaise Kaam Karta Hai?

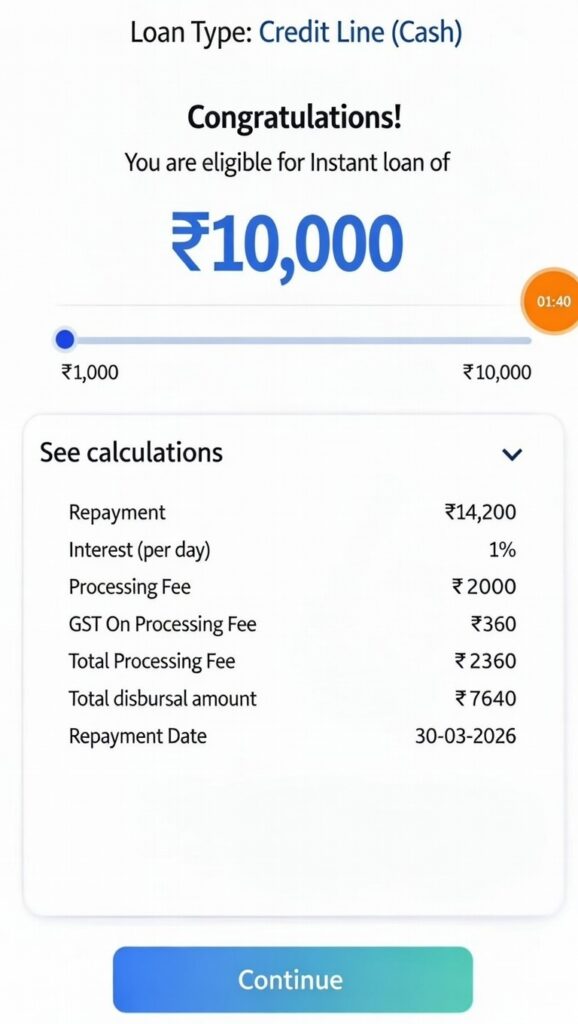

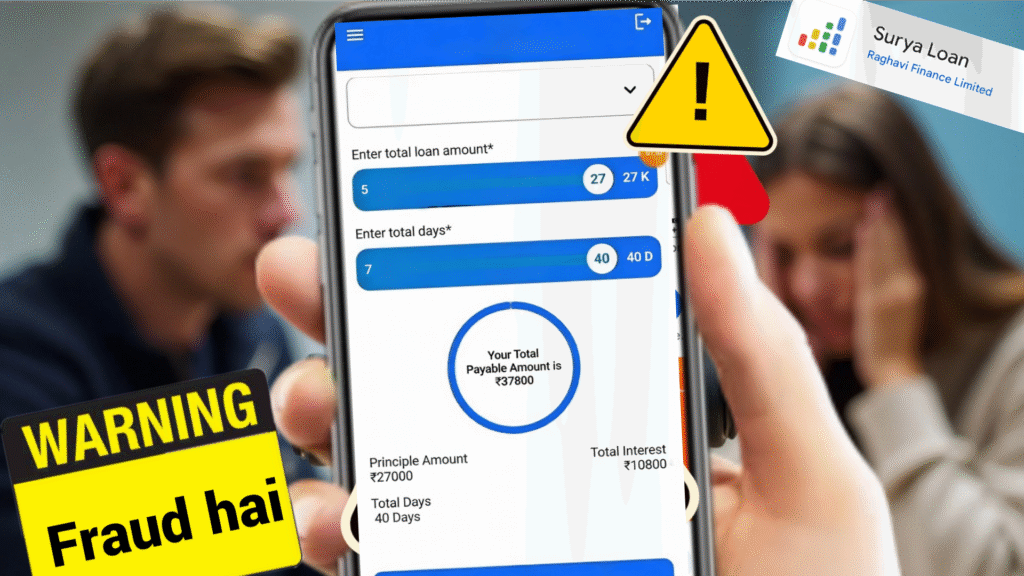

VeyoCredit app ko download karne pe ye claim karta hai ki ye personal credit assistant hai – credit score check karo, budget manage karo, expenses track karo. Lekin real mein users ke according ye instant small loan deta hai, jaise 1500-3000 Rs tak, lekin disbursement kam hota hai (jaise 1800 Rs hi aate hain 3000 ke apply pe). Repayment period sirf 7 days ka hota hai, aur interest + fees milakar amount double ho jata hai – jaise 1800 Rs lene pe 2700-3018 Rs repay karna padta hai.

Ye ek classic 7-day loan app pattern follow karta hai jo India mein bahut common hai fake ya predatory loan apps mein. Official description mein koi interest rate ya fees clearly nahi bataya gaya, sirf “easy credit” aur “secure” bola hai. Lekin users bol rahe hain ki ye hidden charges ke saath aata hai aur repayment time pe harassment shuru ho jata hai.

Play Store Reviews: Critical Users Ki Real Stories

App ki overall rating 4.6 dikhti hai, lekin latest reviews (February 2026 ke) bahut negative hain. Hum yahan kuch real user reviews add kar rahe hain jo aapne share kiye (screenshots se), aur ye bilkul match karte hain typical complaints se:

- Deepika Chauhan (1 star, 20/02/26): “I paid my repayment and one is added in wallet but amount deducted from my account but not showing in wallet in application this is totally fraud please don’t use this application… showing always different vendors and high risk in application.” Ye dikha raha hai ki payment issues hain – paise kat jaate hain lekin wallet mein credit nahi hota, aur app high risk vendors dikhata hai.

- Samuel Jeba (1 star, 21/02/26): “Fraud app. Without consent or approval they credit money in your account. That too only 1500 or 1700 then ask for repayment within 7 days for 2700. Don’t use this app.” Classic unauthorized disbursement – app khud se paise daal deta hai account mein bina permission ke, phir high interest pe wapas maangta hai.

- Alfiya Mulani (1 star, 21/02/26): “Worst ever app, Fraud mene 3000 ka loan approval kiya mujhe account me 1800 hi aaye aur 7 days me repayment karna hai total 3018 rs and they are blackmail on WhatsApp chats and continue calling total fake app.” Blackmail aur continuous calls – ye sabse dangerous part hai. Morph images ya abusive messages bhejte hain recovery ke liye.

- Anil L (1 star, 21/02/26): “Fake app not giving loan only data collection app in 5 second rejected.” Bahut se users bol rahe hain ki loan approve nahi hota, sirf personal data collect karte hain aur reject kar dete hain.

Positive reviews bhi hain jaise Chirag Patel (4 stars): “Really very good easy app” – lekin ye bahut kam hain aur suspicious lagte hain kyunki negative reviews zyada detailed aur consistent hain.

Ye reviews se clear hai ki app heavy charges lagata hai (short term pe 50-100%+ effective interest), 7 days repayment force karta hai, aur agar late hua to harassment shuru.

Kyun Avoid Karna Chahiye VeyoCredit App?

- Heavy Charges aur Short Tenure: 7 days mein repayment, small loan pe bhi interest bahut high – ye RBI guidelines ke against hai jo fair lending promote karte hain.

- Fraud Tactics: Unauthorized credit, blackmail, data misuse – ye predatory lending ke signs hain.

- Developer Location: Indonesia based, India mein RBI registered nahi lagta (koi proof nahi mila legit NBFC ka).

- Play Store Complaints Trend: Bahut se similar apps (jaise fake loan apps) high rating fake reviews se banate hain, lekin real users suffer karte hain.

Agar aapko urgent loan chahiye, to RBI registered apps jaise legitimate banks ya NBFCs (Paytm, MoneyTap, CASHe etc. agar verified) choose karo. Fake apps se bachne ke liye hamesha RBI list check karo.

FAQ: VeyoCredit App Ke Bare Mein Common Questions

Q1: VeyoCredit app real hai ya fake?

A: Real app Play Store pe hai, lekin users ke experiences se ye scam-like behave karta hai – unauthorized loans, high charges, harassment. Bahut se log ise fraud bol rahe hain.

Q2: Isme interest kitna lagta hai?

A: Official mein nahi bataya, lekin reviews se 1800 Rs pe 3018 Rs repay – matlab 60-70%+ charges 7 days mein. Bahut heavy!

Q3: Kya ye RBI approved hai?

A: Koi clear proof nahi mila. India mein digital lending ke liye RBI registration zaroori hai, lekin ye foreign developer ka hai.

Q4: Repayment miss hone pe kya hota hai?

A: Users bol rahe hain WhatsApp pe blackmail, morphed photos, continuous calls. Ye illegal harassment hai – police complaint kar sakte ho.

Q5: Safe hai data ke liye?

A: Reviews mein data collection ke complaints hain, loan reject hone pe bhi info lete hain. Avoid karo personal details dene se.

Q6: Alternative kya use karun?

A: Legit apps jaise Cred, LazyPay, KreditBee (RBI compliant), ya bank apps. Hamesha reviews deeply check karo aur small test karo.

Q7: Agar maine already use kiya to kya karun?

A: Agar harassment ho raha hai, to cyber cell ya police mein complaint karo. Payment mat karo agar blackmail kar rahe hain – ye illegal hai.

Final Thoughts

VeyoCredit app ko avoid karna best hai. Ye ek 7-day loan app hai jo heavy charges lagati hai aur users ko trap karti hai high repayment aur harassment se. Official description attractive hai, lekin critical Play Store reviews sach batate hain – fraud, blackmail, payment issues. India mein fake loan apps ka boom hai, isliye hamesha RBI registered lenders choose karo aur reviews pe bharosa karo.

Agar aapne is app se related experience hai, to comment mein share karo taaki dusre log aware ho sakein. Safe borrowing karo, aur emergency mein family/friends ya legit sources se help lo!