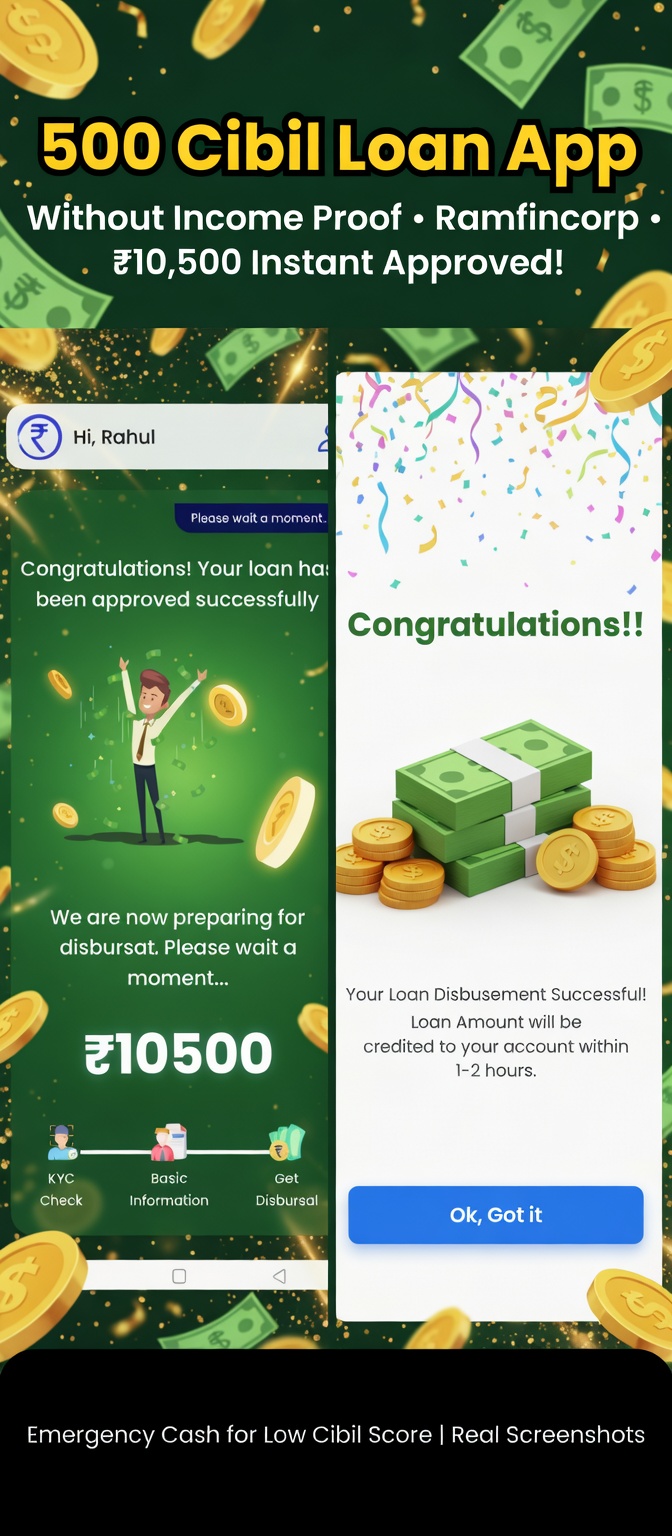

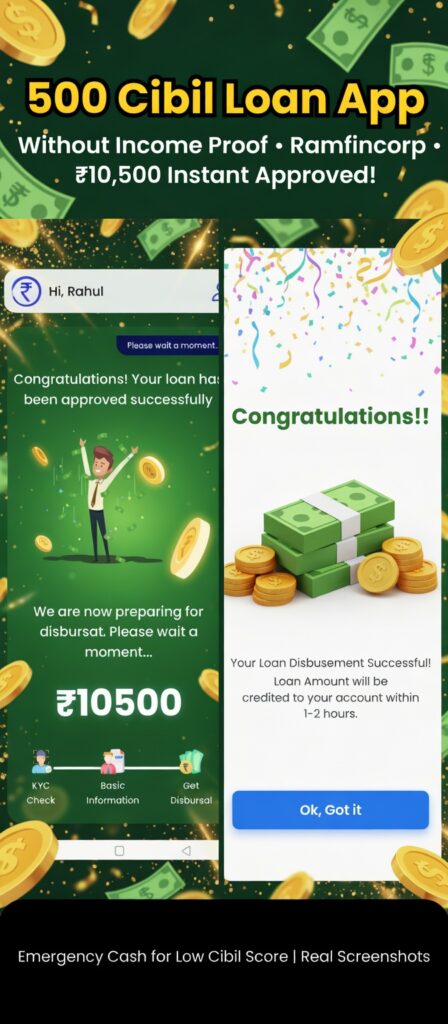

500 CIBIL Score Loan App 2026 Without Income Proof – Best 2 Loan App

Bhaiyo aur beheno, agar aapka CIBIL score sirf 500 hai aur income proof nahi hai, toh 2026 mein bhi tension mat lo! Kai RBI-registered NBFC backed instant loan apps aise hain jo low CIBIL score walon ko bina salary slip ya heavy documents ke loan de dete hain. Aaj hum specially 2 popular apps ke baare mein detail mein batayenge – Cashiva Loan App (yaani CashVia) aur PaapaPay Loan App. Ye dono apps 2026 mein low credit score aur minimal/no income proof ke liye bahut discuss ho rahe hain.

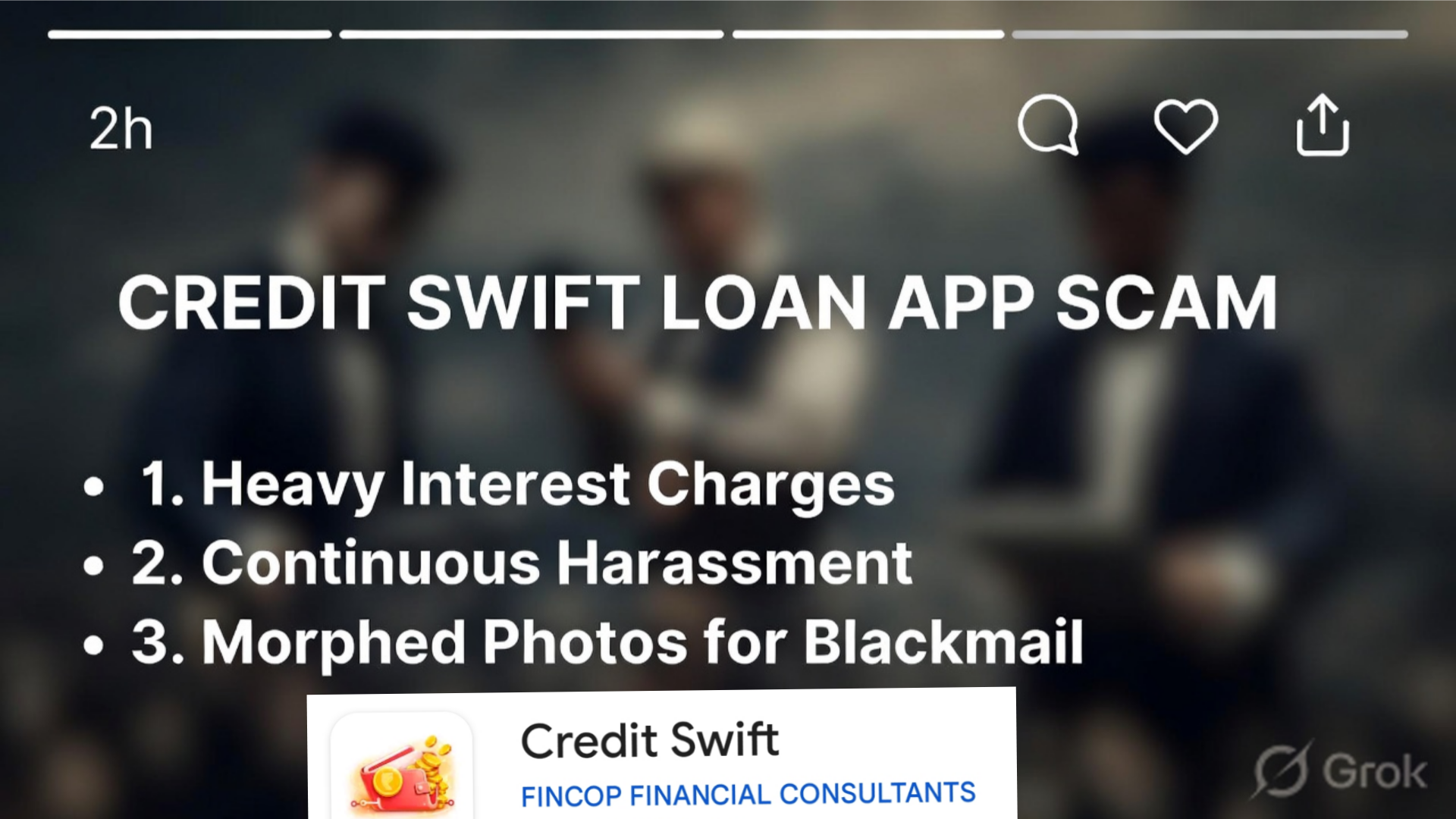

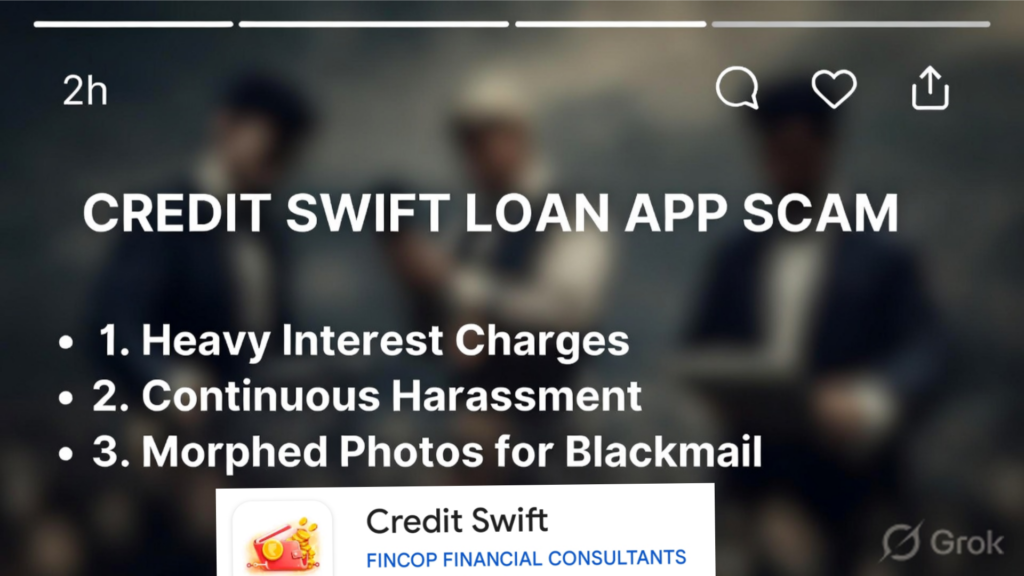

Note: Loan lene se pehle hamesha official Play Store se download karo, RBI list check karo aur apni repayment capacity dekh lo. Interest rates high ho sakte hain, late payment se CIBIL aur kharab ho sakta hai. Ye sirf information hai, financial advice nahi.

1. Cashiva Loan App (CashVia) – Only KYC pe Loan, No Income Proof!

CashVia (jo log Cashiva bolte hain) ek Digital Lending App (DLA) hai jo RBI-registered NBFCs (jaise Grow Money Capital Private Limited) ke through personal loans deta hai. Ye app specially low CIBIL score (500 bhi) walon ke liye bahut popular hai kyunki isme sirf KYC (Aadhaar + PAN) chahiye – income proof ya salary slip ki zarurat nahi padti.

Key Features 2026:

- Loan amount: ₹5,000 se lekar ₹5 Lakh tak

- Interest rate: 1% per month se start (profile ke hisab se)

- Processing fee: 3% (transparent, hidden charges nahi)

- Tenure: 3 se 12 months tak flexible EMI

- Disbursal: Instant approval ke baad minutes mein bank account mein paisa

- Process: 100% online, app download karo → KYC complete → eligibility check → loan apply

Eligibility (bahut simple):

- Age: 18+ (usually 21-60)

- Indian resident, valid PAN & Aadhaar

- Bank account linked

- CIBIL 500 bhi chal jata hai kyunki ye traditional score ke alawa bank transactions aur digital footprint dekhte hain

- No income proof needed (sirf basic verification)

Pros: Bahut fast, minimal docs, high limit tak loan, RBI compliant. 2026 reviews mein log bol rahe hain “low CIBIL pe bhi mil gaya without documents”.

Cons: Interest thoda zyada ho sakta hai agar score low hai. Processing fee alag se.

Kaise Apply Karein?

Google Play Store se “CashVia” search karo, download karo aur apply now button pe click. Bas 10-15 minute mein approval!

2. PaapaPay Loan App – Chhote Emergency Loan, Low CIBIL ke liye Perfect

PaapaPay bhi ek trusted instant loan app hai jo Siddhi Traders Private Limited (RBI-registered NBFC) ke saath kaam karta hai. Ye app small emergency needs ke liye best hai aur 2026 mein low CIBIL score (500 ya usse kam) walon ke reviews mein bahut aa raha hai. Thoda income mention karta hai lekin practical mein alternative verification (bank statement etc.) se kaam ho jata hai.

Key Features 2026:

- Loan amount: ₹500 se ₹20,000 tak (emergency ke liye perfect)

- Interest rate: 3% – 3.25% per month (APR max 233.7% tak – dhyan rakho!)

- Tenure: 62 days se start

- Processing fee: 7.5% + GST se start

- Disbursal: 10 minutes mein bank mein paisa

- Process: Fully digital, PAN + Aadhaar se

Eligibility:

- Age: 20+ years

- Indian resident with PAN & Aadhaar

- Minimum monthly income around ₹25,000 (lekin low CIBIL reviews mein log bolte hain alternative proof se mil jata hai)

- CIBIL low bhi ok – NBFC apna scoring use karta hai

Pros: Bahut chhota loan bhi milta hai, super fast, PAN India available, transparent pricing dikhaata hai pehle se.

Cons: Interest aur fees kaafi high hain chhote loans pe. Bade amount ke liye nahi best. Repay time pe karna zaroori warna penalty.

Kaise Apply Karein?

Play Store pe “PaapaPay” search → download → simple form fill → KYC → instant approval. Website bhi hai: paapapay.in

Final Tip 2026 ke liye

Dono apps mein se Cashiva (CashVia) bada loan chahiye toh best hai (up to 5 lakh, no income proof). Aur PaapaPay chhota urgent paisa chahiye toh. Lekin yaad rakho:

- Hamesha official app se hi download karo (fake apps se bachao)

- RBI website pe partner NBFC check kar lo

- Sirf itna loan lo jitna repay kar sakte ho

- Better option: Pehle CIBIL improve karne ki koshish karo long term mein

Agar aapko in apps ka full review video ya step-by-step guide chahiye toh comment karo. Responsible borrowing karo, paisa samajh ke use karo!

Koi doubt ho toh poochho – main help karunga. Stay safe aur financially strong raho! 💰