VeryCredit – Credit Assistant Loan App Review: Very credit Loan Real or Fake?

Aaj kal India mein instant loan apps bahut popular ho gaye hain. Log jaldi paise chahiye to Play Store se download kar lete hain aur sochte hain ki easy loan mil jayega. Ek aisa hi app hai VeryCredit – Credit Assistant (Play Store link: https://play.google.com/store/apps/details?id=com.verycredit.getscore). Ye app officially claim karti hai ki ye credit score check karne, credit report analyze karne aur personal credit improvement ke liye hai. Lekin real users ke reviews aur experiences se pata chalta hai ki ye basically ek short-term loan app hai, jisme loans mostly 7 days ya usse kam time ke liye dete hain, aur bahut heavy interest rates aur hidden charges lagate hain.

Is article mein hum bilkul honest review denge. Hum app ke official description pe zyada bharosa nahi kar rahe, balki Play Store ke real user reviews aur critical complaints pe focus kar rahe hain. Kyunki description mein to sab kuch perfect dikhta hai, lekin asliyat users ke reviews mein samne aati hai. Ye app bahut se logon ke liye trap ban gayi hai, jahan promised low interest ki jagah actual mein bahut zyada repayment amount maangte hain.

VeryCredit App Kya Hai Aur Ye Kaise Kaam Karti Hai?

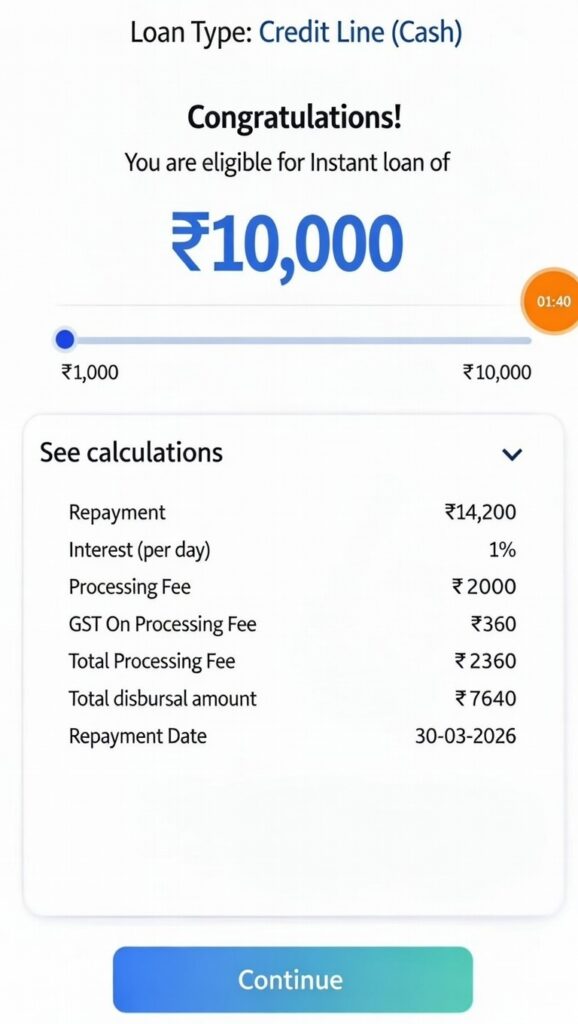

VeryCredit app Play Store pe available hai aur ye “Credit Assistant” ke naam se jaani jati hai. Official description ke mutabik, ye app aapke credit score ko check karti hai, credit report banati hai, aur financial advice deti hai. Lekin users ke according, ye app loan offer karti hai – small amounts jaise 10,000 ya usse kam, aur ye short duration loans hote hain, mostly 7 days ke andar repay karna padta hai.

App download karne ke baad, users apply karte hain, approval milta hai, lekin disbursed amount applied se bahut kam hota hai. Jaise applied 10k ke liye, sirf 2-4k credit karte hain, aur repayment mein double ya triple amount maangte hain. Ye typical predatory loan apps ka pattern hai jo India mein bahut common ho gaya hai.

Critical Reviews Se Sachai Samne Aati Hai

Play Store pe app ki rating shayad high dikhti hai (jaise 4.5 stars), lekin jab aap “Most Relevant” ya low-rated reviews dekhte ho, to bahut serious complaints milti hain. Yahan kuch real user reviews hain jo aapke saath share kar rahe hain (screenshots se liye gaye hain):

- Devendra Pandey (18/02/26, 1 star):

“Total fake app. On ads showing lowest interest rate. While applying it showed me limit 10k then I applied for 10k goes for approval then they showed in their loans approved and they credited 2.4k only and showing repayment of 4k just after 5 days only. In ads they show lowest interest rate. Uske bad jb inhone application fill karwai personal details and kitna loan chahiye bs na interest rate bataya na repayment date btayi bs amount dal di wo meko jitna chahiye tha uska 23% diya fake app.” Matlab: Ads mein low interest dikhaate hain, lekin actual mein sirf partial amount dete hain aur bahut high interest (23% jaise) lagate hain short time mein. - Laxmi Gupta (20/02/26, 1 star):

“They disbursed only 3700 but the repayment amount is 6700….that much they are taking… very worst thing and also they are giving only 6 days..” Yahan clear hai – 3700 diye, 6700 maange, sirf 6 days mein. Ye almost 80-100% interest short period mein! - Gopi Tadisetty (22/02/26, 1 star):

“Fake app 3000 loan amount transfer only 1800 repayment only 6 days collect the 3000 amount only interest 1200.” Applied 3000, sirf 1800 mile, 6 days mein 3000 repay + 1200 interest. Bahut heavy charges! - Kuch positive reviews bhi hain jaise “very easy and very fast to use” (Sisir Sing, 4 stars), lekin ye zyadatar generic lagte hain aur critical reviews ke muqable kam helpful votes paate hain.

Ye reviews February 2026 ke hain aur bahut similar complaints hain: Disbursed amount kam, repayment double/triple, short tenure 5-7 days, ads mein low interest dikhaate hain lekin actual mein heavy charges.

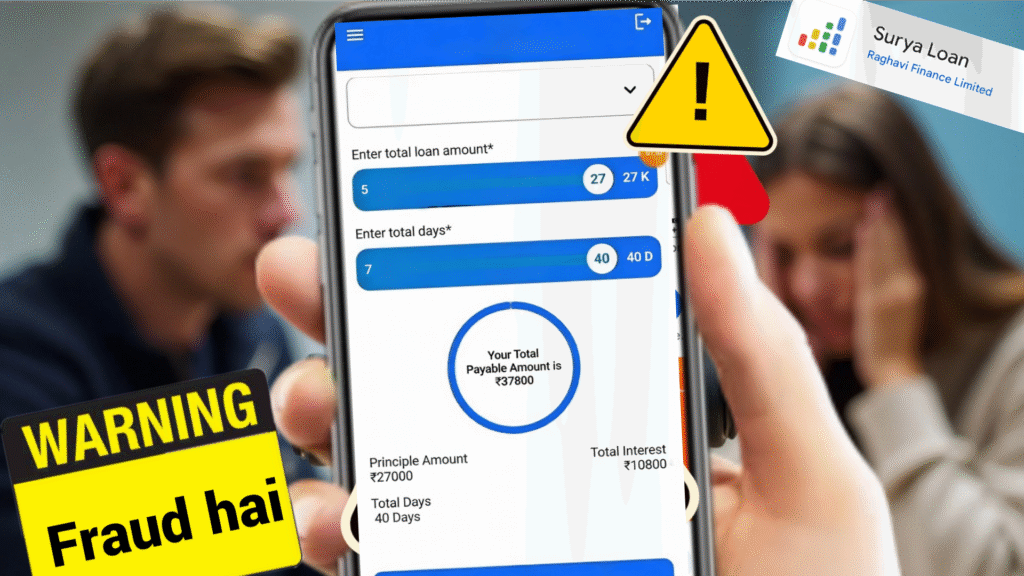

Kyun Ye App Heavy Charges Lagati Hai?

VeryCredit jaise apps short-term (7 day) loans deti hain, jo basically payday loans jaise hote hain. Inme interest rates bahut high hote hain kyuki tenure bahut kam hota hai. India mein RBI guidelines ke according legitimate apps ko max 36% APR aur minimum 60 days tenure follow karna chahiye, lekin ye apps ye rules bypass karte hue dikhte hain.

Users kehte hain:

- Ads mein attractive low interest dikhaate hain.

- Approval ke time actual terms nahi batate.

- Disbursement ke baad high repayment maangte hain.

- Agar late ho to harassment ya extra charges.

Ye pattern India ke bahut se fake/illegal loan apps mein common hai, jahan log trap ho jaate hain aur mental stress face karte hain.

Risks Aur Side Effects

- Financial Trap: Chhota loan lete ho, lekin repay karne ke liye double paise chahiye, jo cycle ban jaata hai.

- Privacy Issues: App personal data, photos, contacts access maangti hai, jo misuse ho sakta hai.

- Harassment: Kuch cases mein late payment pe threats aate hain (though is app ke specific mein itna mention nahi, lekin similar apps mein hota hai).

- Credit Score Impact: High interest default karne se credit score kharab ho sakta hai.

Better hai ki aise apps se door rahein. Agar loan chahiye to banks, NBFC jaise Bajaj Finserv, MoneyTap, ya RBI-approved apps use karein.

Alternatives Kya Hain?

- Bank Apps: SBI YONO, HDFC, Axis – low interest personal loans.

- Trusted Apps: Paytm Postpaid, LazyPay, CASHe – better terms.

- Government Schemes: Mudra Loan ya Stand Up India for small business.

Hamesha RBI registered lender check karein aur reviews carefully padhein, specially 1-star wale.

FAQ – VeryCredit Loan App Ke Baare Mein Common Questions

Q1: VeryCredit app real hai ya fake?

A: App Play Store pe hai, lekin users ke reviews se ye predatory lending karti hai. Description credit assistant ka hai, lekin actual mein high-charge short loans deti hai. Bahut se log ise fake ya scam bolte hain.

Q2: Isme interest rate kitna hota hai?

A: Official mein low interest claim, lekin reviews mein 20-100%+ effective rate short 5-7 days mein. Jaise 3700 pe 6700 maangna almost 80% charge.

Q3: Loan kitne din ka hota hai?

A: Mostly 7 days ya usse kam (5-6 days common reviews mein).

Q4: Kya ye safe hai use karna?

A: Nahi recommended. Heavy charges, hidden terms, aur potential harassment ke risks hain.

Q5: Agar already loan liya hai to kya karein?

A: Repay karne ki koshish karein, agar harassment ho to cybercrime.gov.in pe report karein ya police complaint.

Q6: Play Store se remove karwaya ja sakta hai?

A: Agar bahut complaints aaye to Google remove kar sakta hai, lekin abhi available hai.

Q7: Better options kaun se hain?

A: RBI-approved apps ya direct bank loans – lower interest aur transparent terms.

Conclusion: VeryCredit – Credit Assistant ek aisa app hai jo attractive ads se attract karta hai, lekin real users ke critical reviews se clear hai ki ye 7 day loan app hai jo bahut heavy charges lagati hai. Description pe bharosa mat karo, reviews padho aur avoid karo. Financial emergency mein trusted sources se hi loan lo, warna problem badh sakti hai.