In today’s fast-paced world, especially in a country like India where unexpected expenses can hit anyone at any moment—be it a medical emergency, a sudden repair bill, or bridging a salary gap—short-term personal loans have become a lifeline for many. Among the numerous instant loan apps flooding the Google Play Store, DigiCredit stands out as one that promises quick, paperless financial help. Marketed as a Digital Lending App (DLA) partnering with RBI-registered NBFCs like Khosya Finlease Private Limited, it targets salaried individuals looking for hassle-free borrowing.

But is it really as smooth as the advertisements claim? In this comprehensive article (over 1200 words), I’ll dive deep into what DigiCredit offers, its features, eligibility, pros and cons, and—most importantly—real user experiences, including the ones shared in the screenshots you provided. I’ll keep it straightforward, balanced, and human, like a friend who’s researched this thoroughly before advising you.

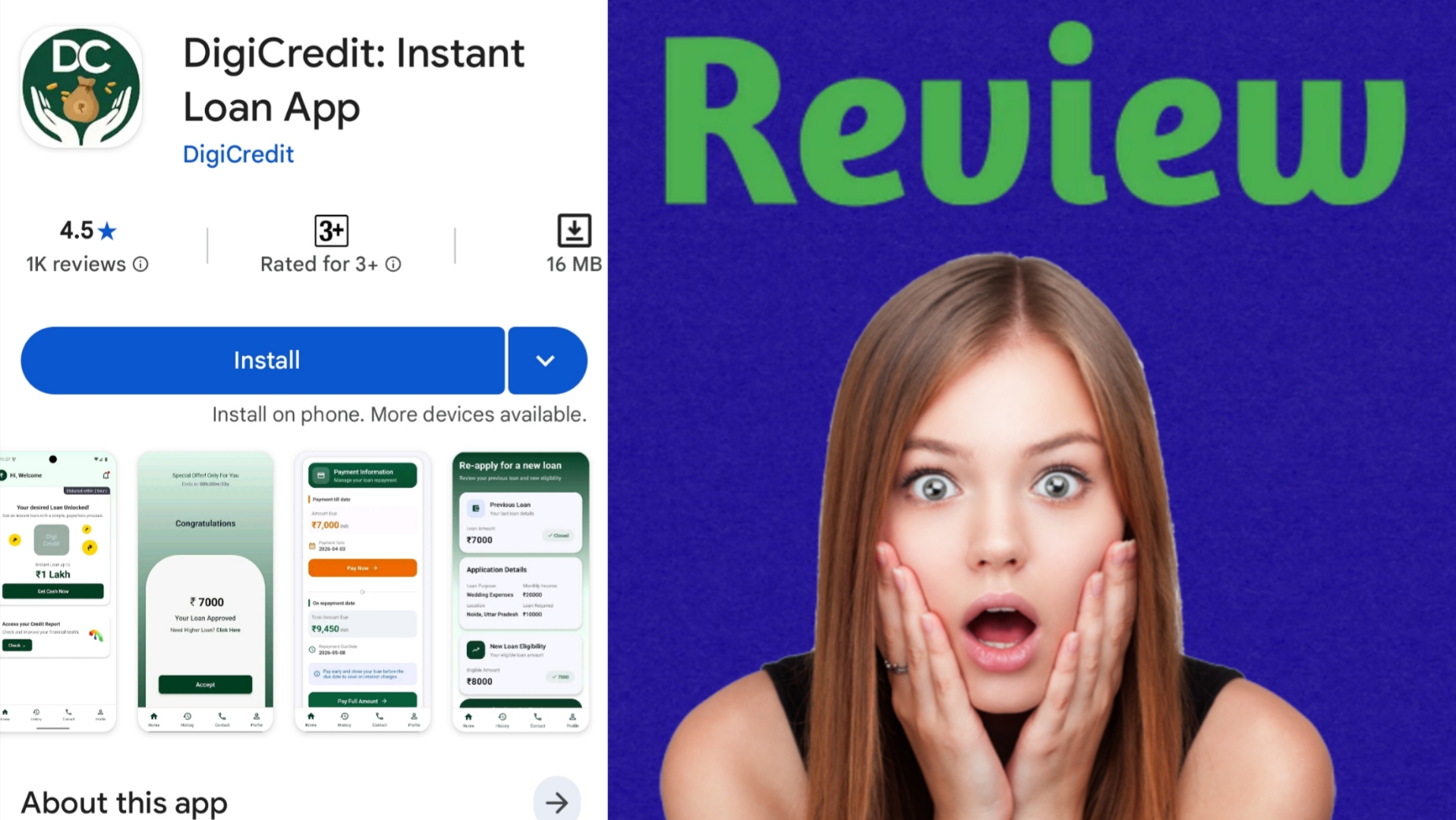

What is DigiCredit Loan App?

DigiCredit is an instant personal loan application available on the Google Play Store. It acts as a platform connecting borrowers with lending partners rather than lending money directly itself. According to its official listing, the app focuses on small-ticket, short-to-medium-term loans designed for urgent needs.

Key loan details include:

- Loan Amount: ₹1,000 to ₹50,000 (some promotions mention up to ₹1,00,000, but standard is lower).

- Tenure: Typically 62 to 120 days (though you mentioned 30-40 days in your query—some users report shorter effective cycles due to processing or specific offers).

- Interest Rate: Up to 36% APR (Annual Percentage Rate), plus processing fees up to 10% + GST.

- Disbursal: Claimed to be quick, often within minutes to hours after approval, directly to your bank account.

The process is 100% digital: Download the app, complete KYC with Aadhaar and PAN, provide basic details like income proof, and get an instant eligibility check. It’s targeted at Indian residents, aged 21-55, primarily salaried people with a decent credit profile.

The app highlights benefits like minimal documentation, no collateral, and transparency. Their website and social media push messages like “Get funds in minutes” and “Hassle-free loans for emergencies.” With a 4.5-star rating on Play Store (from 100K+ downloads), it looks promising at first glance.

How Does the Application Process Work?

- Download and Signup: Available on Android. Users register with mobile number and verify OTP.

- KYC & Eligibility: Upload documents. The app uses algorithms to check creditworthiness.

- Loan Application: Select amount and tenure. e-NACH (Electronic National Automated Clearing House) mandate is often required for repayment.

- Approval & Disbursal: If approved, funds hit your account quickly.

- Repayment: Auto-debit via mandate or manual options. Early closure might have restrictions.

Sounds simple, right? But as we’ll see from user stories, the reality can be quite different.

The Good Side: When It Works

Many users appreciate the speed for genuine small needs. Positive aspects often mentioned in reviews (not shown in your images but common in aggregates):

- Truly paperless for eligible candidates.

- Available even for those with moderate CIBIL scores (though amounts are smaller).

- Useful for short-term gaps, like 1-3 months.

- Partner NBFC is RBI-registered, adding some legitimacy compared to shady unregulated apps.

If your credit is strong, income stable, and you repay on time, it can be a convenient option in a pinch.

The Reality Check: Common Complaints and User Experiences

However, scrolling through recent reviews paints a concerning picture. Your provided screenshots highlight recurring issues that many borrowers face. Let’s break them down honestly—these aren’t isolated; they echo across forums and YouTube reviews.

1. Disbursement Delays and False Approvals

Multiple users report that the app shows “Loan Approved” and even completes e-mandate, but the money never arrives on time—or at all.

From one review in your images (Gurupreet Kaur, 23/03/26): “Very poor as they show loan approval is done but disbursement never happened… no money transferred in my bank.” She mentioned requesting cancellation but still seeing the loan in her account.

Another user (Amol Vanjire): “They call to apply for a loan, and after applying they make e-mandate compulsory and deduct money. After that, they show the amount as disbursed, but it does not come on time. This is a fraud company.”

This pattern—approval shown, mandate signed, but delayed or missing funds—frustrates people who need money urgently.

2. Poor Customer Support and No Response

This is one of the biggest pain points.

Soarabh’s review (19/03/26): “They don’t have any customer care. Only they can call you, you don’t. They cancel my loan after the disbursement, even eNACH process also was complete. They asking me to mail here, but there are 20+ mails which they didn’t replied.” He initially thought they weren’t a scam but called it the “worst available loan application.”

Soumya Ranjan Padhan echoed this: No updates, calls not connecting, no response to emails, and loans not disbursed after approval. He strongly advised against using it.

Manjunath BR (31/03/26): “Complete fraud application. The customer care people aren’t professional at all. You can’t close the loan early. The app keeps giving you error and the customer care doesn’t respond at all.”

3. Repayment and Credit Score Issues

Even when things go right initially, problems arise later. Praseedha Balan (04/05/26) shared: “I have repaid the loan on time but credit report still showing overdue 24000… I have also sent the mail for the same.” This can damage your CIBIL score badly, making future borrowing harder.

4. Other Frustrations

- High effective costs due to processing fees and short tenures.

- App glitches preventing full process.

- Aggressive calls or mandates without clear communication.

- Difficulty in early closure or modifications.

“Just Chiil” mentioned applying and waiting 12+ hours with no disbursement, noting other platforms are faster.

These reviews come with company responses apologizing and promising to look into issues, but users often say follow-ups don’t lead anywhere.

Is DigiCredit Safe or a Scam?

It’s not an outright illegal scam—it’s linked to a registered NBFC and follows basic RBI digital lending guidelines (no loans below 62 days in their policy). However, the operational issues—delays, unresponsive support, and credit reporting errors—make it feel unreliable for many. High interest + fees can make small loans expensive quickly (e.g., a ₹10,000 loan could cost significantly more over 2-3 months).

Pros:

- Easy digital process for eligible users.

- Quick approval for some.

- Transparent terms on paper.

Cons:

- Frequent disbursement failures.

- Terrible customer service.

- Risk to credit score.

- High costs for very short needs.

- Inconsistent user experience.

Who Should Consider DigiCredit?

Only if:

- You have a strong credit profile.

- You need a small amount and can repay strictly on time.

- You’ve read all terms, including fees.

- You’re okay with potential delays.

Better Alternatives: Compare with established players like Bajaj Finserv, Moneyview, or bank apps (e.g., SBI, HDFC) which might have better support and lower effective rates for salaried people. Always check latest RBI guidelines on digital lending.

Final Verdict and Advice

DigiCredit positions itself as a savior for instant cash needs in India, but real-world experiences—like the ones in your screenshots—suggest caution. Many users feel trapped between approval promises and actual delivery, leading to stress rather than relief. While some get their loans smoothly, the volume of complaints about non-disbursal, ghost customer care, and post-repayment issues is too high to ignore.

Tips Before Applying to Any Loan App:

- Read full terms, especially fees and mandate clauses.

- Check your CIBIL first.

- Borrow only what you can repay comfortably.

- Keep screenshots of every step.

- Have backup plans—family, salary advance, or formal banks.

- File complaints on RBI’s Sachet portal or consumer forums if issues arise.

If you’re in Indore or anywhere in India facing a genuine short-term crunch (30-40 days), think twice before jumping on DigiCredit. Explore multiple options and prioritize platforms with proven track records. Financial decisions should bring peace, not anxiety.

This app might work for a lucky few, but based on widespread feedback, it’s far from the seamless experience they advertise. Stay informed, borrow responsibly, and protect your credit health—it’s your most valuable financial asset.